AT- A Glance |

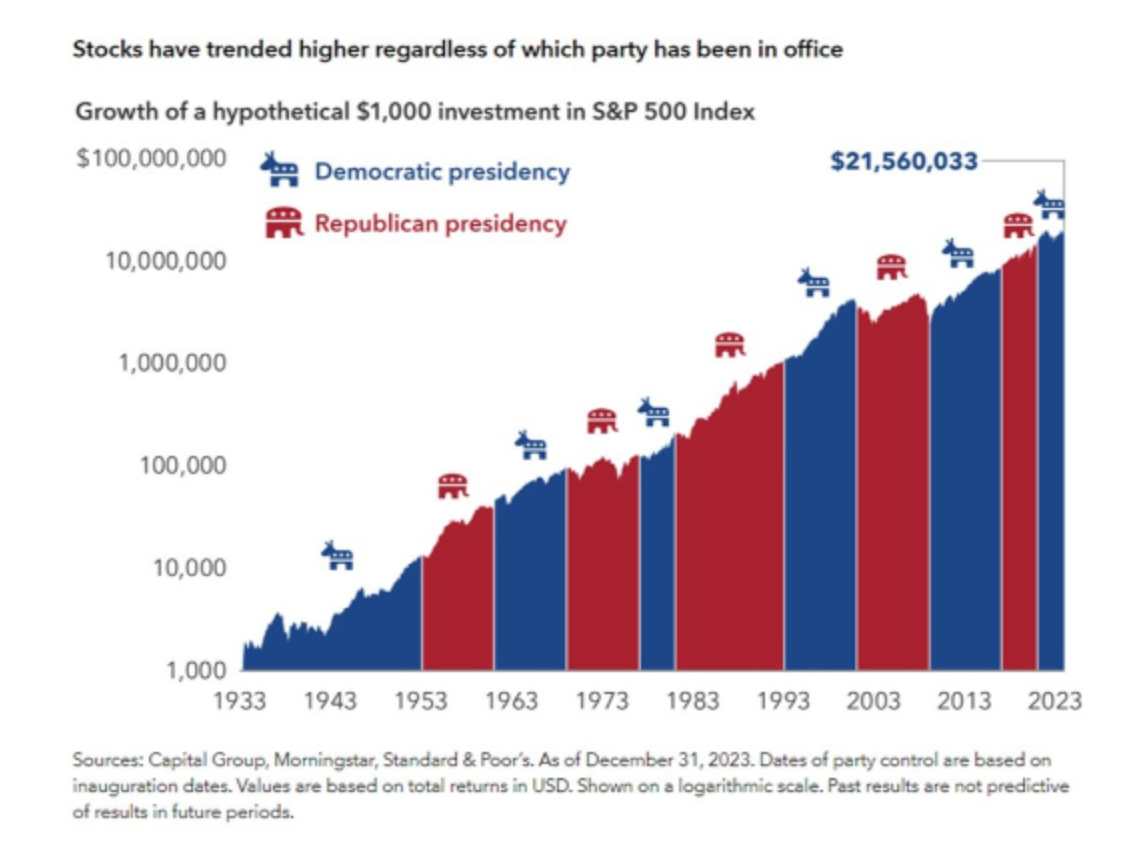

The Investment Committee met on the afternoon of Monday, August 5th. In mid-July, the S&P 500 index reached a new all-time high before falling back as we neared month's end. Over the last week, the combination of the Federal Reserve Bank not lowering interest rates at its July meeting combined with a disappointing unemployment report sparked levels of market volatility that we had not seen since the 2020 COVID-19 crisis. Our committee members reviewed these recent events and the outlooks of the various economists and market strategists we follow. As we watched markets continue to rise in recent months, our committee reminded you in our June 10th report that trees don’t grow to the sky, and some bouts of volatility and pullback were likely in the near term. “As we move towards the summer months, the political conventions, and the upcoming elections in the fall, we would not be surprised to see some additional volatility arise.” We have seen this play out over the last week, as the S&P 500 index pulled back approximately 8% while technology and small-cap stocks both moved into correction territory, dropping more than 10%. This volatility was largely driven by the combination of the Federal Reserve Bank once again not lowering interest rates at its July meeting last week. The Fed puts out its Summary of Economic Projections on a quarterly basis. In both December and March, they indicated that they would likely cut interest rates three times this year. This initially led to an upturn in the markets, as investors expected lower interest rates to spark economic growth and higher corporate profits. However, after raising interest rates for the 11th time in July 2023, the Fed has gone a full year and has not cut the rates yet. This stands in contrast to other major central banks, such as the European Central Bank, the Bank of England, and the Bank of Canada, which have all started lowering interest rates as global inflation pressures have continued to moderate. After the Fed decision on Wednesday last week, the Bureau of Labor Statistics released its monthly unemployment report on Friday. The expectation was for 180,000 new jobs to be created. The actual number of new jobs came in at a disappointing 114,000, much lower than expected. At the same time, the unemployment rate, which had bottomed at 3.4% in April ‘23, unexpectedly rose to 4.3%. We are also seeing weekly unemployment claims, a leading economic indicator, continue to rise. This combination of real interest rates remaining at a restrictive level, while employment measures continue to point towards a slowing labor market has sparked concerns of recession. This led to a significant downturn in the markets on Friday and Monday. The Volatility Index, also known as the VIX, jumped to its highest level since the 2020 COVID-19 pandemic. Recent geopolitical events in the United States, the Middle East and South America have also added to investor unease. Against this backdrop, the committee would like to remind you of a couple of things. First, all the committee members continue to receive questions about the impact of the upcoming election on the markets and the economy. As you can see from our first chart below, provided to us by our friends at Capital Group, markets have typically rewarded investors under various presidential administrations over the last 80 plus years, despite of which party was in control of the White House. Some did better than others, but this is a strong illustration of why staying with your diversified investment portfolio, despite alarming headlines, generally makes good sense.

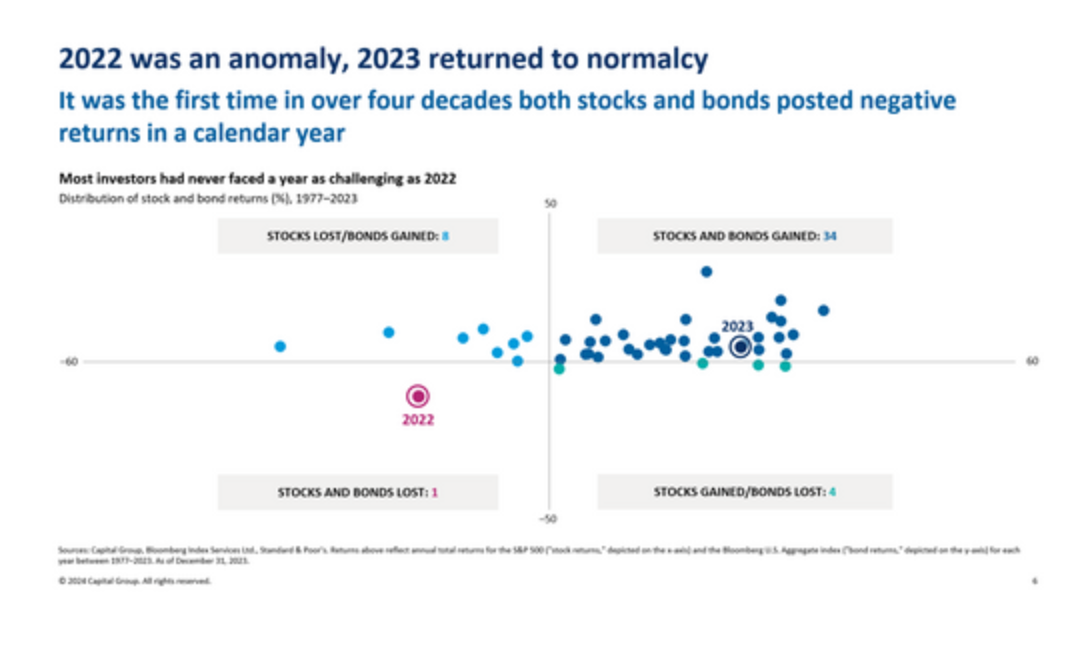

We would like to remind you that, despite who wins the election, technology companies will continue to make smartphones and invest in AI, pharmaceutical companies will continue to create and manufacture new drugs to help manage disease, and consumer brand manufacturers will continue to produce the toilet paper and Raisin Bran you consume. Typically, once the uncertainty of an election cycle has passed, the leaders of great American companies will have a better understanding of the tax and regulatory policy they must contend with and will adjust accordingly. The second thing we would like to remind you is that time-tested investment tools such as diversification and regular rebalancing continue to be prudent strategies for many investors to consider and help us manage your hard-earned investment assets. Many people look back to 2022, when both stock and bond prices fell at the same time, and question whether diversification will work in the future. Our second chart below shows what an anomaly that year was. It was the only time since 1977 that stocks and bonds fell at the same time.

This means that as the stock market has pulled back recently, diversifying assets, such as bonds and gold, have moved up, thereby offsetting some of the losses we have seen in the equity markets. Rebalancing portfolios, where you sell certain assets that have done well at a higher price to buy assets that have fallen recently and are on sale, is also a useful strategy during these times. Final ThoughtsFinally, we would like to remind you that market downturns are the financial equivalent of a sale. We know that Americans love to buy anything they can at lower prices. We can look at Black Friday and Prime Days for evidence. Unfortunately, most Americans don’t take advantage of lower prices when they see the value of their investment portfolio temporarily drop. We would like you to remember the eternal wisdom of Warren Buffett, who said: "Be fearful when others are greedy and to be greedy only when others are fearful." As always, the committee members and your advisor are here to help guide you if you have questions about your unique situation. Please do not hesitate to reach out. We appreciate your continued support and trust, especially in times of heightened uncertainty. Have a great day! Should you have any questions regarding these notes, please do not hesitate to contact Kevin at (678) 401-6102 |

The views stated in this piece are not necessarily the opinion of Cetera Advisors LLC and should not be construed directly or indirectly as an offer to buy or sell any securities. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. |