December 2024 Investylitics

Horizon Advisor Network Investment Committee December 9, 2024

Executive Summary

- The markets are experiencing a lot of optimism in the wake of the outcomes of the 2024 elections. This is partly due to expectations of the 2018 tax cuts being extended and a friendlier regulatory environment for the business community.

- Moderating inflation expectations and positive outlooks for GDP and earnings growth have contributed to the market achieving 56 new all-time closing highs this year, the fifth-most since 1929.

- There are some concerns about stock market valuations being stretched. However, this is primarily influenced by the Mag 7 and AI stocks' outsized weighting in traditional stock indexes. While not cheap, equal-weighted and smaller-cap indexes are more in line with historical valuation measures, while many international indexes are discounts.

- Job growth rebounded somewhat in the latest employment report. This, along with some components of inflation proving stickier and a more optimistic growth outlook for next year, could limit the number of interest rate cuts the Federal Reserve Bank may be able to enact.

- With markets near all-time highs, we would not be surprised to see some pullbacks or bouts of short-term volatility. Maintaining the disciplined diversification created by your advisor and rebalancing your portfolio regularly remains the preferred approach during such times.

The Horizon Advisor Network Investylitics Committee members met on the afternoon of Monday, December 9th, to continue to evaluate the post-election investment and economic landscape. The markets are experiencing a lot of optimism in the wake of the outcomes of the 2024 elections. This is partly due to expectations of the 2018 tax cuts being extended and a friendlier regulatory environment for the business community. This has led many of the market strategists and economists we follow to update their outlooks and provide some insight as to what we can expect as we move toward 2025.

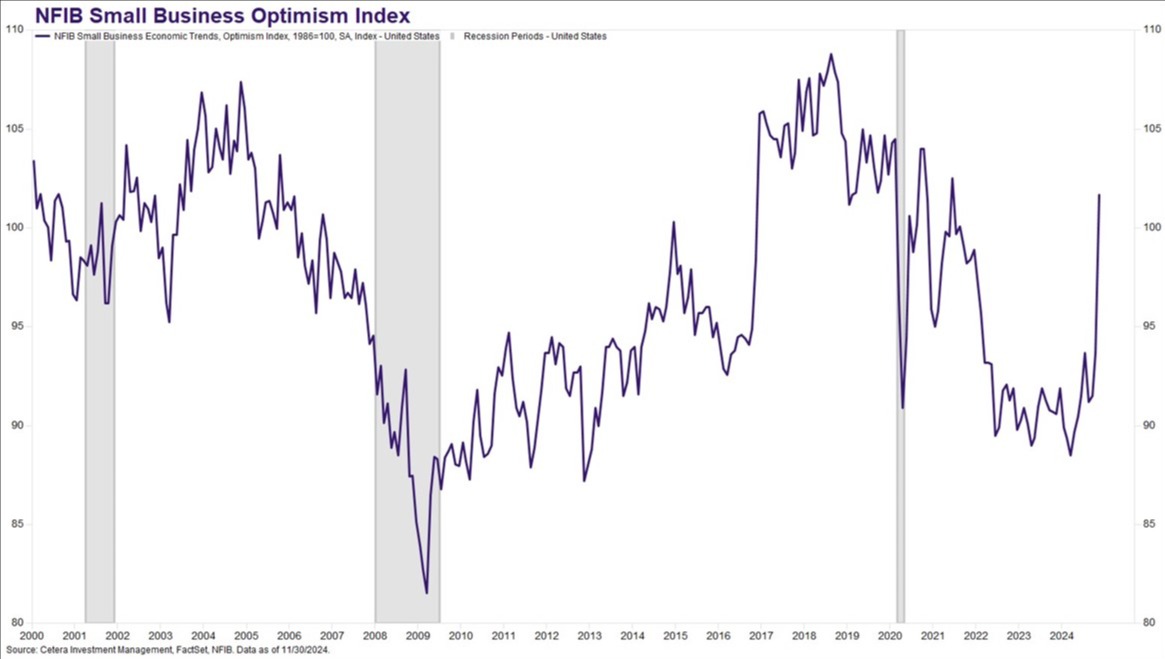

This positive sentiment is clearly visible in our first chart below. The NFIB Small Business Optimism index surged to a 41-month high of 101.7 in November, driven by a 41-point improvement in the percentage of owners expecting the economy to improve. If you look closely at the chart, you will notice that the last time we saw a surge in small business optimism like this was eight years ago in the wake of the 2016 presidential election. While sentiment improved post-election, inflation and the high costs remain the top concerns for small business owners.

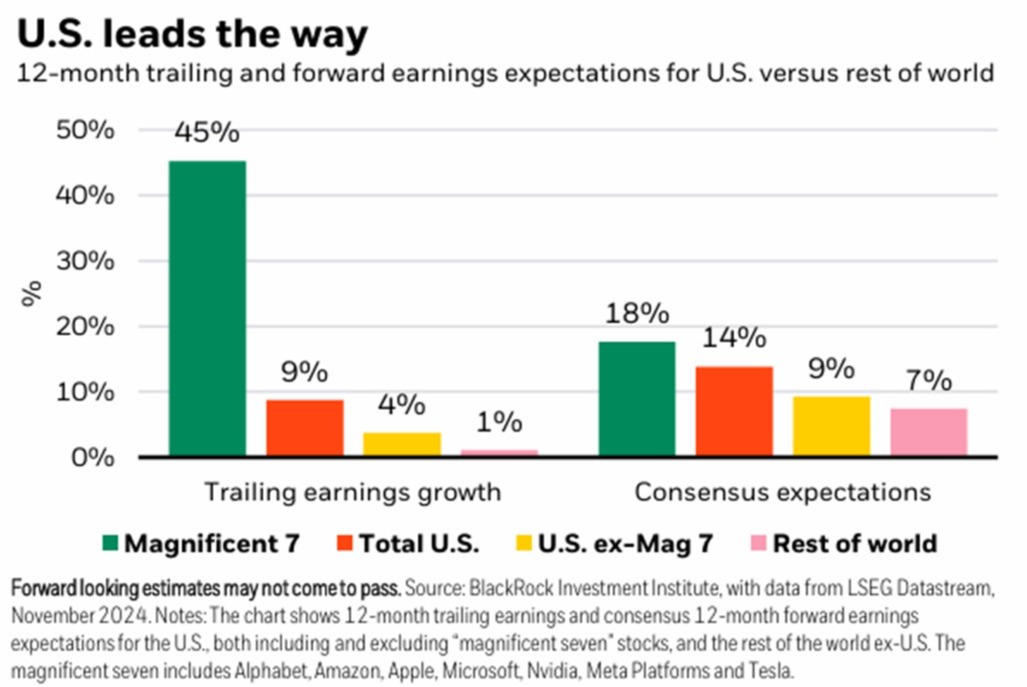

There are some concerns about stock market valuations being stretched. However, this is primarily influenced by the Mag 7 and AI stocks' outsized weighting in traditional stock indexes. Though not cheap, equal-weighted and smaller-cap indexes are more in line with historical valuation measures, while many international indexes are trading at discounts. This likely means that further gains in the stock market will be driven primarily by earnings growth rather than by expanding multiples. For the time being, you can see in the chart below that earnings in the United States are projected to continue to lead the world in the next year. The committee will closely be watching whether or not these relatively rosy projections actually come to fruition and continue to support stock prices.

All eyes will be on the Federal Reserve Bank meeting next week, which will conclude on Wednesday, December 18th, at 2:00 PM. They are expected to announce an additional 25 basis point interest rate cut, its third of the year. The Fed will also release its updated Summary of Economic Projections. This will show the outlook of the various Federal Reserve Bank Regional Presidents and Fed Governors regarding GDP growth, inflation, unemployment, and further interest rate cuts in the new year. Job growth rebounded somewhat in the latest employment report. This, along with some components of inflation proving stickier, as well as a more optimistic growth outlook for next year, could limit the number of interest rate cuts the Federal Reserve Bank may be able to enact.

Against this backdrop, the economy continues to grow at or above trend expectations. Despite several recession indicators pointing toward an economic downturn in 2024, this has yet to materialize. This can largely be attributed to US consumers continuing to show resilience. Consumer spending and retail sales continue to surprise to the upside, which has contributed to positive economic growth and corporate earnings. Despite growing tensions in the Middle East, low gas prices continue to fuel holiday cheer, averaging under $3 per gallon nationwide. At just 9.6% of average hourly earnings, gas affordability is well below the 20-year average of 13.4%, which provides a tailwind for consumers during the holiday season.

With markets near all-time highs, we would not be surprised to see some pullbacks or bouts of short-term volatility. If and when that occurs, we should not be deterred, nor should we allow our faith in our well-conceived and constructed wealth accumulation plans to be shaken. We have seen this movie before and understand that volatility is part of the admission we pay to get long-term capital growth. We planned for this, and with markets near all-time highs, we should have actively created the liquidity we need to ride out temporary drops in the stock market.

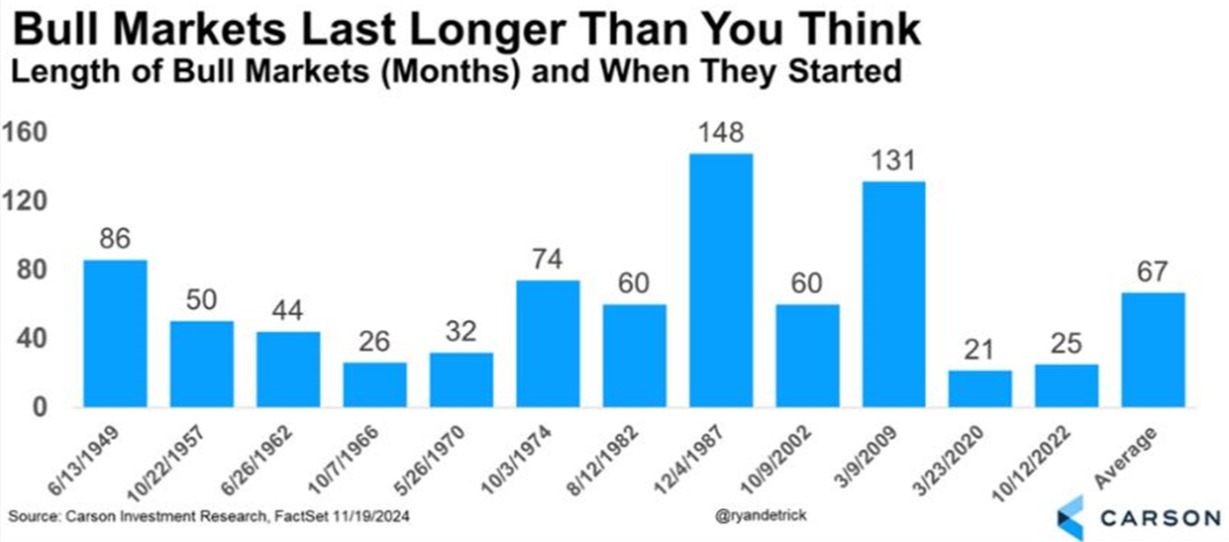

By the way, the bull market we are experiencing is still relatively young by historical standards. As you can see in our final chart below, we are approximately 25 months into this stock market upturn. The average length of a bull market has been more than five years since the end of World War II.