February 2025 Investylitics

Horizon Advisor Network Investment Committee February 10, 2025

Executive Summary

- The U.S. stock market built on last year's strong performance, with the S&P 500 rising by a very solid 2.8% in January. This bodes well for the remaining months of 2025 as over the last three decades, the index returned an average of 16% during years in which it increased in January.

- Many of the economists and market strategists that our committee follows have noted that valuations on the stock market appear to be stretched. However, this has been driven by a handful of tech/AI stocks. By contrast, the equal-weighted index is trading much closer to historical norms.

- All eyes will be on this week's CPI and PPI inflation reports and Jay Powell’s congressional testimony on Capitol Hill. The Fed paused its interest rate-cutting campaign at its January meeting and signaled that it is willing to be patient until it has better data on inflation and unemployment trends in the new year.

- Economic indicators continue to point toward an economy growing at or above historical trend levels. Near-term recession risk seems to be relatively low, as 9 of the 12 indicators on ClearBridges' recession dashboard turned positive.

- While we know that daily headlines and policy uncertainty can drive volatility in the short run, we still believe that a diversified asset allocation and regularly rebalancing your portfolio are the best tools to help manage risk in this environment.

The Horizon Advisor Network Investylitics Committee members met on the afternoon of Monday, February 10th. Given the flow of economic data and the flurry of policy initiatives from the new administration, there was a lot to consider as we continued to evaluate the investment and economic landscape.

The S&P 500 advanced 3% in January despite rising bond yields and a notable tech sector decline. Historical trends suggest that early-year gains often set the tone for above-average annual returns. Over the past three decades, years with positive January performance have delivered an average return of 16%, while years with a negative January return resulted in an average annual return of about 3%.

Many of the economists and market strategists that our committee follows have noted that stock market valuations appear to be stretched. However, this has been driven by a handful of tech/AI stocks. As you can see on the left side of our first chart below, the forward-looking price-to-earnings ratio of the S&P 500 index has been trading more than one standard deviation above the historical norm for the last 15 years.

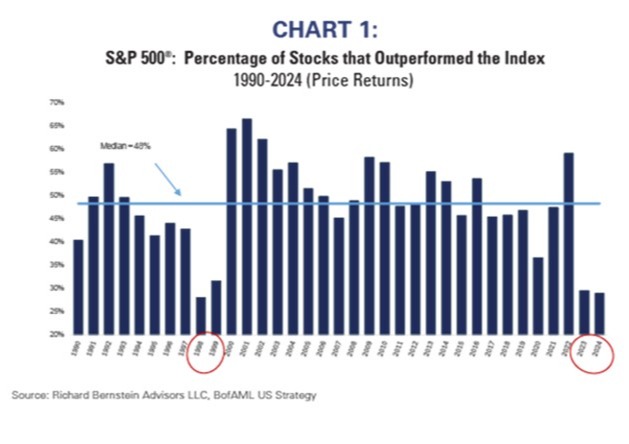

By contrast, the equal-weighted index on the right is trading much closer to historical norms. This suggests there may be opportunities in other parts of the market with lower valuations. This is further evidenced by the small number of stocks that have exceeded the index returns recently. As you can see from our second chart below, less than 30% of stocks outperformed the index in the previous two years. You will also note that the last time we saw a similar occurrence was in the late 90s in the lead-up to the internet and dot com bubble.

All eyes will be on this week's CPI and PPI inflation reports and Jay Powell’s congressional testimony on Capitol Hill. The Fed paused its interest rate-cutting campaign at its January meeting and signaled that it will be patient until it has better data on inflation and unemployment trends in the new year.

The market is trying to understand and digest the new administration's policy initiatives as we move forward. These include extending the current tax cuts, deregulation, a pro-growth business environment, cutting government spending, reducing energy prices, reducing immigration, and implementing additional trade tariffs.

A recent comment from Jared Franz, an economist at Capital Group and the American Funds, gives us a reasonable summation of these issues:

It’s still unclear what the final effective tariff rates will be, to which goods they will apply, and when or if they will be implemented. In my view, Trump is more concerned with the reaction from the U.S. stock market than he is with the bond market. That may rein in his inclination to impose crippling trade barriers for extended periods of time. With this in mind, I stand by my optimistic assessment. I expect the U.S. economy to continue on a path toward healthy expansion in 2025, roughly in the range of 3% GDP growth.

Economic indicators also continue to point toward an economy growing at or above historical trend levels. Near-term recession risk is relatively low, as 9 of the 12 indicators on ClearBridges' recession dashboard turned positive.